2026 Environment | Threat Vectors & Effects on Business

Main Takeaway Points

Seven independent threat vectors are converging simultaneously in 2026: over a trillion in maturing debt, sweeping tariffs, energy shocks, supply chain fractures, critical industrial disruptions, a weakening consumer base, and a traditional credit blackout.

The supply side carries the majority of the exposure. Demand will contract in pockets but will not disappear. It flows toward the prepared.

Hidden inflation is rising on all sides of the transaction simultaneously, incentivizing conservatism and compressing microeconomic activity.

Operationally, this presents as a slower season initially. If multiple vectors converge on a single business in a short window, distress becomes a likely outcome.

The collective margin for error is shrinking. Buyer delays, volatile traffic, and supply chain disruptions are compressing cash flow margins across the board.

On the buy-side, loan maturities, tariffs, and supply volatility are incentivizing enterprise buyers to delay payables and renegotiate terms aggressively.

On the sell-side, rising input costs and energy prices are forcing sellers to demand faster receivables and raise prices to protect margins.

The buyer-seller relationship is under structural strain. Larger, more liquid enterprises hold leverage over smaller businesses who cannot absorb the pressure.

Dead inventory risk is elevated. A single missing sub-component from an energy rationed Asian factory can ground an entire domestic production line regardless of where the majority of materials are sourced.

Corporate layoffs are accelerating through automation. Re-hiring is occurring predominantly toward offshore labor, reducing domestic purchasing power further.

Businesses that stay aware, reposition proactively, and build asymmetrical networks will hold a structural advantage over those operating reactively.

Alternative vendor networks, expanded buyer surface area, and access to private capital channels are the foundational moves for surviving and positioning within this environment.

Table of Content

Executive Overview

Section I | General Landscape

Section II | Threat Vectors

Section III | Effects on Businesses

Section IV | Strategies for Preparation

Conclusion

About Eieyani Capital Associates

References

Disclaimer

Executive Overview

The global economy in 2026 is not experiencing a standard cyclical downturn.

It is a structural convergence of multiple independent threat vectors colliding simultaneously, and the combined pressure is fundamentally different from any single recession or correction a business owner has navigated before.

The Strait of Hormuz closure in March 2026 triggered an immediate energy shock that is still rippling through every layer of physical commerce. [1] Sweeping U.S. tariff regimes have quietly installed a hidden consumption tax on domestic businesses. [2] Over one trillion dollars in commercial real estate and private equity debt is maturing under interest rates that make refinancing mathematically devastating. [3] Global supply chains are fracturing at the sub-component level, creating shortages that hit without warning. [4] Consumer spending is decelerating under a record $18.8 trillion household debt load. [5] And traditional banking channels have retreated from the real economy at the exact moment businesses need liquidity most. [6]

Each of these pressures would be manageable in isolation.

Together, they create a compounding environment where the margin for error has effectively disappeared for unprepared operators.

The danger is not obvious. This environment disguises itself as a slow season, a tough quarter, a few delayed payments. By the time the full weight of it lands on a business, the window to respond proactively has already closed.

A single bad month under these conditions can erase years of hard-earned equity.

The redeeming reality is that fundamental demand has not disappeared. Infrastructure, manufacturing, healthcare, construction, and essential services continue to operate. The businesses that survive and capture ground in this cycle are the ones that understand what is coming, protect their core, and position themselves before the disruption hits their specific sector.

This report below exists to give you that clarity.

Section I | General Landscape

Economic uncertainty has been escalating since the start of 2026, and the conditions driving it are not isolated. The closure of the Strait of Hormuz in March triggered an immediate energy shock that is still compounding across every layer of physical commerce. [1] U.S. tariff regimes have installed a silent consumption tax on domestic businesses importing the materials they need to operate. [2] Over a trillion dollars in commercial real estate and private equity debt is maturing under interest rates that make refinancing mathematically punishing. [3] AI integration is actively displacing white-collar employment, stripping purchasing power from the consumer base that small and mid-sized businesses depend on. [7] And the cost of living refuses to relent, pushing households into pure survival mode and pulling discretionary spending out of the economy.

These pressures are not arriving one at a time. They are converging simultaneously, and that convergence is what makes this environment structurally different from any standard cyclical correction a business owner has navigated before. An isolated economic strain forces inefficiency out of the market and rewards disciplined operators. A multi-variable convergence of this scale does not correct cleanly. The lingering effects will persist for months to years even if a full diplomatic resolution in the Middle East were achieved tomorrow. The physical infrastructure damage, the repriced debt, the depleted supply buffers, and the exhausted consumer balance sheets do not unwind overnight.

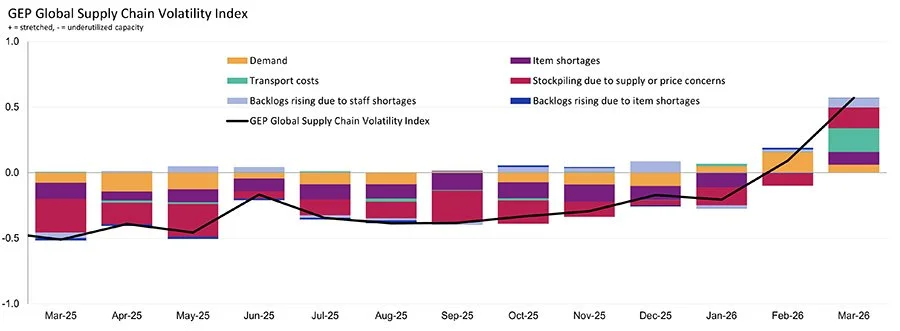

The full weight of these combined shocks has not fully landed yet. The primary disruptions originated in Eastern trade corridors, and a structural lag is masking the damage. [4] Current inventory buffers and goods already in transit are creating a false sense of stability across several sectors. That buffer is depleting. The convergence point for Western markets is projected between the end of Q2 and the start of Q3 2026, and when it arrives, it will hit simultaneously across industries rather than sequentially.

On the ground, the pattern is already visible for operators paying attention. B2B buyers are aggressively delaying payables to hoard cash, citing their own supply chain pressures as justification. B2C foot traffic and digital conversion rates are dropping 20–40% depending on the sector. Suppliers are raising prices and shortening payment terms at the same time. The operator in the middle absorbs pressure from both directions with a cash buffer that was not built for this duration of stress.

The deeper systemic risk compounds this further. If the Strait remains blockaded past Q3, crude oil futures contracts must settle against a physical inventory that cannot support them. [8] The paper market snaps upward violently. The institutions holding those contracts manage capital on behalf of pension funds, insurance frameworks, corporate treasuries, and high-net-worth families. A forced clearinghouse liquidation at that scale passes catastrophic losses straight down to the working class and through every business dependent on those consumers spending.

The most dangerous feature of this environment is how quietly it arrives. It presents initially as a slow season, a few delayed payments, a slightly softer quarter. The hidden strain does not surface until a specific disruption hits: a key buyer defaults, a critical material goes into shortage, a vendor raises prices without warning. [9] At that point the business is already in distress, and the window to prepare proactively has closed.

The redeeming reality is that fundamental demand has not disappeared. Infrastructure, construction, manufacturing, healthcare, and essential services are still operating and still require vendors, suppliers, and service providers to function. The market in this cycle will reward the operators who protected their cash, mapped their exposures, and built relationships with alternative capital and supply sources before the pressure arrived. For those already feeling the squeeze, actionable defensive protocols still exist. The window is narrowing, but it is not closed.

Section II | Threat Vectors

Threat Vector I | Loan Maturities

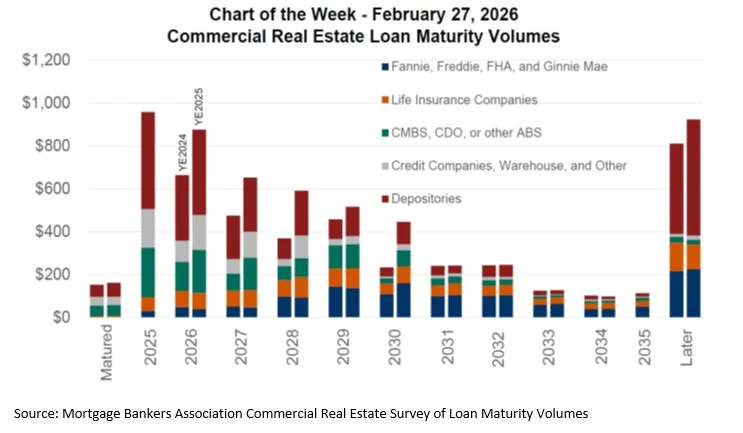

Over one trillion dollars in legacy corporate and real estate loans are maturing right now, concentrated heavily in commercial real estate ($800–900 billion) and private equity acquisition debt ($350 billion). [3] These loans were originally written at near-zero interest rates following COVID. Refinancing them at today's 8% market rates is a completely different mathematical reality. Property valuations collapse under the new debt structure, and PE-backed companies that were profitable at 4% interest are now operating at break-even or negative margins at 9%. [10]

The institutional response to this pressure flows directly down to everyday businesses. Landlords facing refinancing gaps immediately stop paying vendors on time. Net-30 payment terms get pushed to Net-90 or longer as commercial property owners hoard cash to survive their own debt crisis. Private equity firms running distressed portfolios execute the same playbook across their supply chains: they demand faster payment from their clients while extending their own payables to vendors as far as possible. The result is a structural vice. Small and mid-sized businesses get squeezed from both directions simultaneously, their enterprise buyers slowing down payments while their enterprise suppliers demand faster ones. The cash flow disruption is not a sign that any individual business is failing. It is the mechanical output of a high-finance debt problem landing on the pavement of the real economy.

Threat Vector II | Global Tariffs: The Silent Border Squeeze

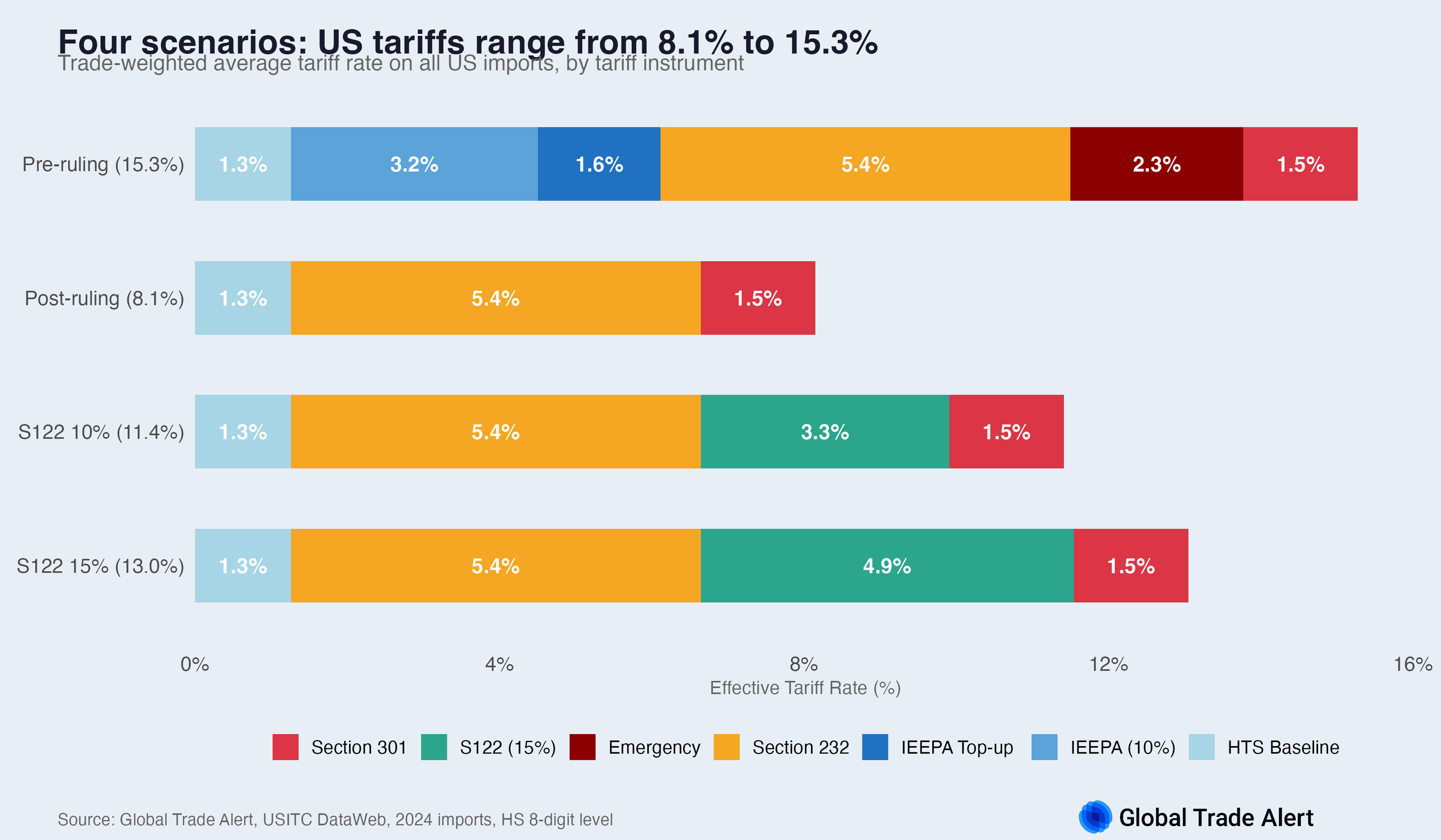

The U.S. government has deployed a multi-layer tariff regime with the stated goal of reshoring domestic manufacturing. [2] Section 122 adds a 15% global emergency surcharge. [11] Section 232 adds national security penalties on steel and aluminum. [12] Section 301 locks in an additional 25% penalty on Chinese manufacturing. [13] Stacked together, European imports face combined surcharges up to 40%, and Chinese goods face compounding penalties that have fundamentally repriced entire product categories.

The operational reality is direct: foreign exporters do not pay these duties.

Domestic businesses importing goods pay at the border, and that cost passes through every layer of the supply chain before landing on the operator running the business. A freight operator sees truck parts costing 50% more than two years ago. A precision parts manufacturer in the Midwest cannot pass tariff costs to clients who have hardcapped pricing, and domestic mills cannot match the technical specifications of the Canadian steel they depend on. A construction subcontractor sees materials up 25–50% while operating on budgets that were locked in 2024. The domestic reshoring infrastructure needed to eliminate this pressure does not exist yet and cannot be built overnight. [14] Until the sub-tier supplier networks are established on domestic soil, these tariffs function as a permanent, compounding hidden tax on the businesses running today.

Threat Vector III | The Energy Market’s Physical Shortages and Paper Liquidation

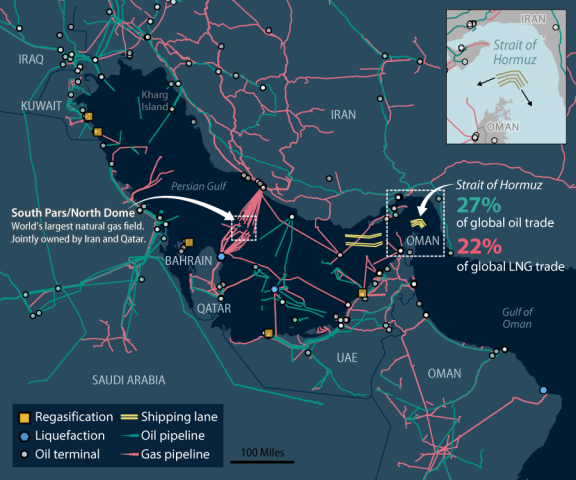

The closure of the Strait of Hormuz cut off approximately 20% of the world's seaborne energy exports overnight. [1] Oil benchmarks are pinned in a $90–120 per barrel range, with a serious risk of violent upward movement. The core problem is that global refineries were built to process medium and heavy Middle Eastern crude. American light shale cannot simply substitute into those refinery configurations. Pumping more domestic oil does not solve a structural infrastructure mismatch. [15]

Beneath the physical shortage sits a second, less visible threat: the paper derivatives market. Trillions of dollars in futures contracts are approaching hard expiration deadlines in Q2–Q4 2026, and a massive volume of institutional capital has bet on a diplomatic resolution that has not materialized. [8] If those contracts expire against depleted physical inventory, the paper market is forced to settle against reality. Prices snap violently upward, potentially into the $150–200 range, triggering forced institutional liquidations that will pass straight through pension funds, insurance frameworks, and corporate treasuries down to the ground floor of commerce.

For business owners, elevated energy costs are already locked in regardless of how diplomacy unfolds. Every physical input costs more to produce, move, and store. A solo trucking operator sees a single mechanical failure become a liquidation event when diesel-inflated margins leave no buffer. A restaurant absorbs both the logistics surcharge and a food cost spike driven by fertilizer shortages, with no ability to double menu prices without losing the customers they still have.

Threat Vector IV | Global Supply Chain Fragility & Sub-Component Cascade

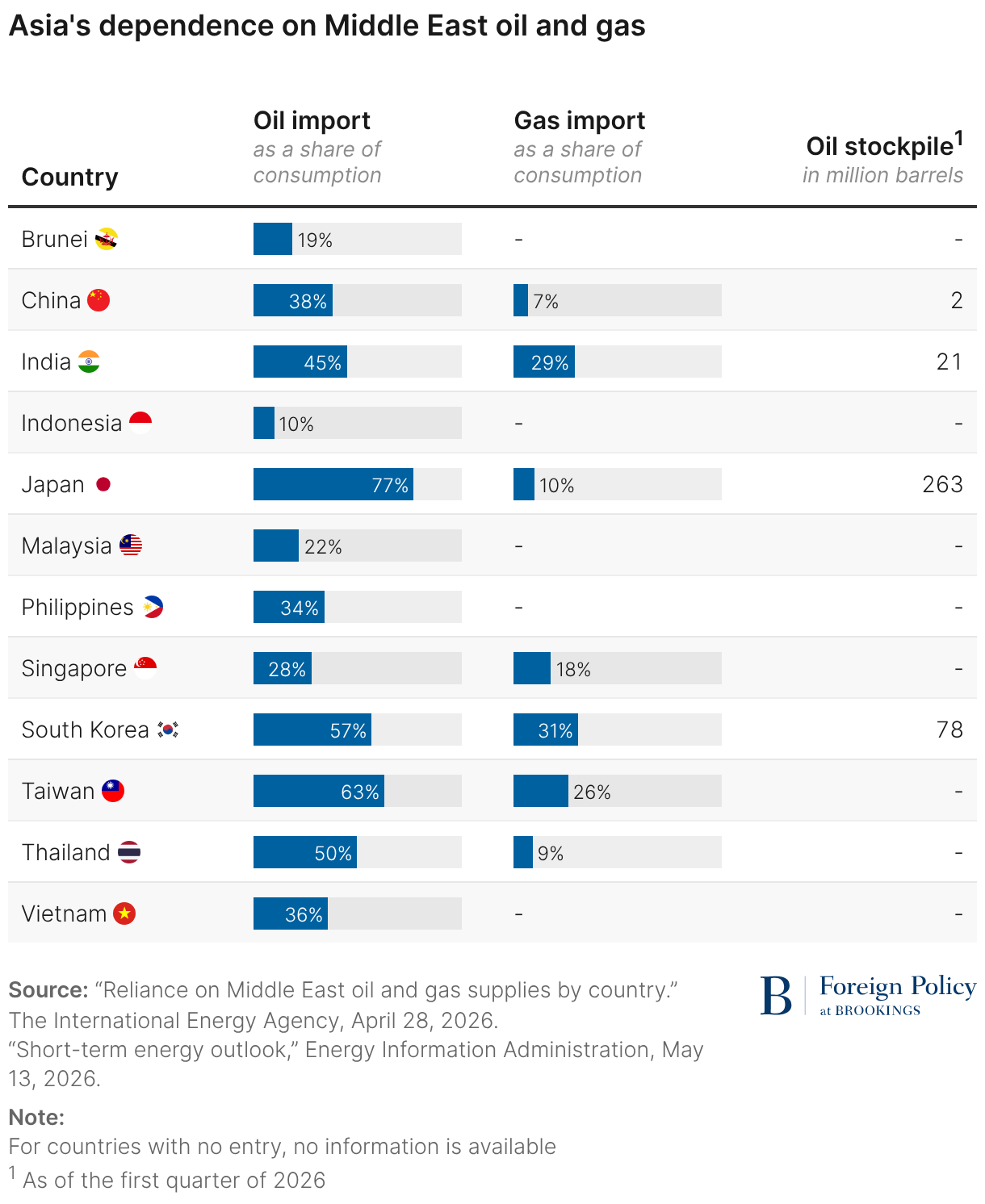

The Strait closure exposed the foundational dependency of global manufacturing on concentrated energy corridors, and the fracture point is not where most operators expect it. It is not in primary materials. It is in the sub-components: the $0.05 resistors, the $5 microchips, the specialized fasteners produced exclusively by small and mid-sized factories across East and Southeast Asia. Those factories are now operating on energy rationing, some with as little as four hours of power per day. [16] Their output is collapsing. [4]

The result is dead inventory at scale. A Texas manufacturer with domestic steel and aluminum sitting on the floor cannot ship a completed product because a single Electronic Control Unit from a rationed Vietnamese factory has not arrived. A Sacramento aerospace manufacturer faces 40-day shipping delays on European specialty metals rerouted around the Cape of Good Hope, while being locked into firm-fixed-price government contracts that allow zero cost pass-through to the Pentagon. A consumer goods brand absorbs a 30–50% spike in polymer packaging costs because petrochemical feedstocks tied to Middle Eastern naphtha have gone into shortage. The fatal blind spot for most operators is that they only manage two layers of their supply chain: their direct vendor and their direct buyer. The disruption is happening three and four tiers back, completely invisible until it arrives as an unexpected price hike, a missed delivery, or a vendor declaring force majeure. By that point, the operator's cash flow is already in crisis.

Threat Vector V | Disruption in Critical Industries & Upstream Breakdown

The energy crisis is not only disrupting finished goods supply chains. It is breaking the foundational industrial inputs that every physical product depends on: petrochemicals, basic chemicals, industrial metals, and polymer plastics. These are not niche materials. They are the raw building blocks of modern commerce, and their production is concentrated in facilities that governments are now actively rationing power to protect. [17]

The structural divide is the core problem. State authorities across East Asia, Europe, and the Middle East are directing scarce energy to the top 1–2% of mega-conglomerates deemed critical to national economic survival. The remaining 98% of the industrial ecosystem, the Tier 3 through Tier 6 specialty manufacturers, distributors, and regional precision producers, are left to survive on residual power. These are the exact companies that produce the specialized inputs the protected giants need to build their own flagship products. The paradox is self-defeating, but the rationing continues regardless.

For North American operators, the transmission mechanism is invisible until it hits. A regional produce distributor operates on stable current inventory while the fertilizer shock from disrupted ammonia supply quietly decimates spring planting acreage. [18] The supply cliff does not arrive until autumn harvest, by which point the distributor is locked into fixed-price contracts they cannot renegotiate. A mid-market logistics firm watches port freight volumes drop as maritime detours add 20 days to every Asia-to-Europe voyage, leaving trucks idle and fixed equipment notes still due. A medical equipment manufacturer holds millions in devices that are 99% complete and 100% unsellable because a German alloy supplier went into an unannounced 45-day shutdown due to energy rationing. The lag time built into this crisis is its most dangerous feature. [9] Businesses are operating today on inventory buffers that mask the underlying shortage. When those buffers clear, the disruption hits the entire market simultaneously.

Threat Vector VI | Consumer Base Weakening and the Household Debt Increasing

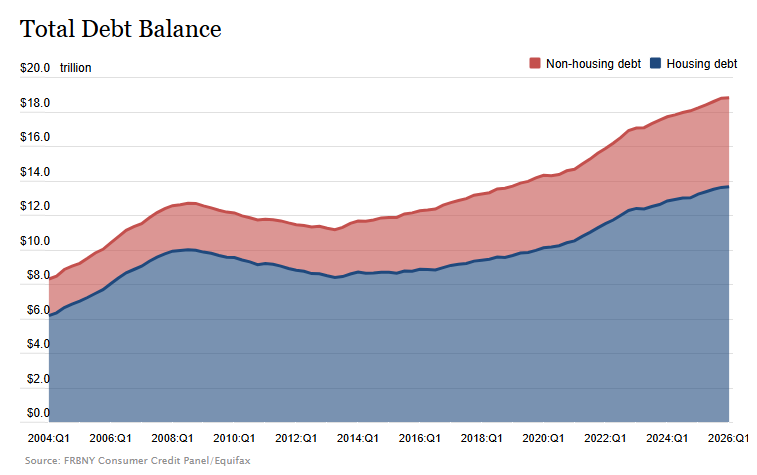

U.S. household debt reached a record $18.8 trillion in Q1 2026. [5] Mortgages, auto loans, student debt, credit cards, and consumer lines are all elevated simultaneously, and the delinquency rate, while appearing stable at 4.8%, sits on top of a base that has zero remaining margin for additional stress. Consumers are already in survival mode. Foot traffic is inconsistent, retail velocity is slowing, and sentiment indices are at historic lows. [19]

The compounding pressure is corporate automation. Large conglomerates are actively cutting white-collar and middle-management positions in favor of automated systems, which improves their margins but removes purchasing power from the exact consumer class their revenue depends on. [7]

The structural paradox is real: the largest companies are systematically degrading the spending capacity of their own customer base. For SME operators, the consequence is direct. A neighborhood restaurant sees foot traffic become sparse and unpredictable while ingredient costs rise from tariff-laden supply chains and utility bills climb from energy surcharges. To survive, it cuts hours and staff. Those displaced workers now face their own fixed debt obligations with reduced income, further pulling back on discretionary spending and tightening the regional economic loop. A commercial cleaning firm gets squeezed identically from both directions: B2B landlords push payables to Net-60 and Net-90 to protect their own cash, while B2C residential clients cancel discretionary services to manage household budgets. The firm must still pay its workers weekly in real-time cash. Revenue is frozen in receivables. The cash flow mismatch is not a business model failure. It is the mechanical output of a consumer base that has run out of buffer.

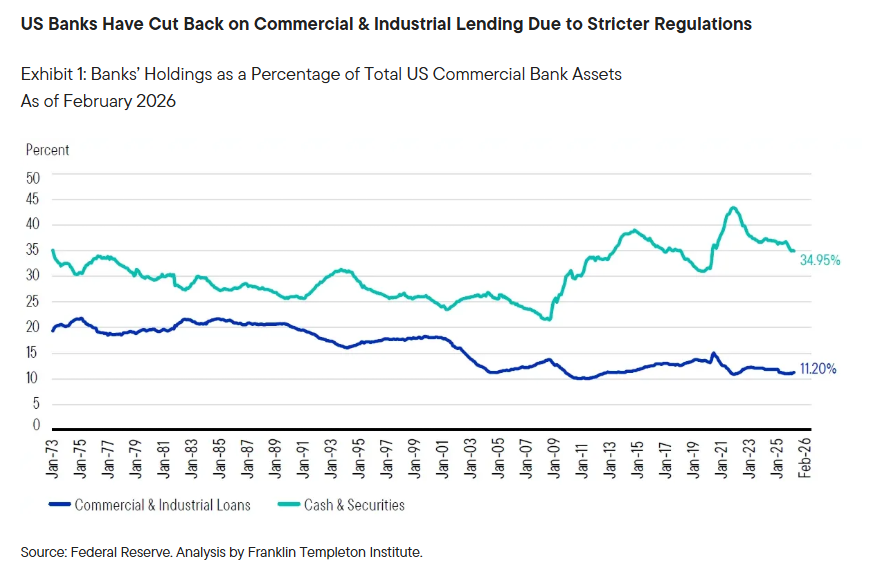

Threat Vector VII | The Credit Blackout & Inaccessible Lending

Traditional banks have retreated from the real economy. Basel III capital requirements, combined with balance sheets clogged by underperforming commercial real estate debt, have forced institutional lenders into deep risk aversion. [6] Regional banks briefly stepped into the gap with record C&I loan originations in early 2026. The Middle East escalation and energy volatility ended that momentum. The lending pie is physically shrinking as deposit bases contract under fractional reserve mechanics.

The private credit market holds $1.5–2 trillion in undeployed capital, and it is largely inaccessible to the businesses that need it. [20] Institutional funds require minimum ticket sizes of $5 million and above.

The smaller private lenders operating in the $100K–$5M range exist but are decentralized, hidden, and require a level of financial packaging expertise most operators do not have. Capital is abundant globally and completely offline locally. The consequence for businesses caught in a liquidity crunch is a forced path toward predatory alternatives. A Seattle apparel brand absorbs Vietnam energy rationing costs, gets auto-declined by a regional bank, secures an MCA to stay alive, and watches daily ACH debits consume the remaining margin until a minor revenue dip triggers default and liquidation. A Chicago metal fabrication firm with strong contracts and a decade of operational track record gets pushed to break-even by Net-90 buyer payment cycles. A PE firm identifies the distress, acquires 51% at a steep discount, strips the assets, and exits. [21] A Nashville utility contractor with 20 years of municipal relationships and hundreds of skilled employees gets outbid at a loss by a mega-conglomerate with institutional capital access, poached of key staff, and ultimately forced into a distressed sale at a fraction of its true value. These businesses did not fail because their models were broken. They failed because structured capital was unavailable at the moment they needed it, and the only alternatives on offer were designed to accelerate their collapse.

Section III | Effect on Businesses & Strategies

Viewed from a distance, the scale of these threat vectors can create a sense of paralysis. The numbers are large, the dynamics are global, and the language of debt walls and futures liquidation can feel disconnected from the reality of running a business day to day. The operational truth is more grounded. This is a large structural restructuring, not an extinction event. Most businesses will not face all seven threat vectors simultaneously. The danger is the ones you do not see coming, because this environment specializes in blindsiding operators who are otherwise executing well.

The pattern is consistent across every example in this report.

A fundamentally healthy business absorbs one shock, then a second, then a third, each individually survivable, until the cash buffer is gone and the next disruption has nothing to land on. A delayed payment from a major buyer is manageable with reserves. Combined with a material cost spike and a revenue dip from softening consumer demand, it becomes a liquidity crisis. The business was not broken. It was unhedged.

The only durable response to this environment is awareness, adaptability, access, and accountability. Awareness means understanding which of these vectors interact with your specific sector before they arrive. Adaptability means being willing to reposition operations, renegotiate terms, and adjust cost structures without waiting for the crisis to force it. Access means having direct lines to capital, alternative vendors, and demand channels before you need them urgently. Accountability means owning every decision with the clarity that the macro environment does not excuse poor execution, and preparation does not guarantee survival but dramatically improves the odds.

Nothing in this environment rewards passivity. The businesses that will capture displaced market share over the next 12 to 24 months are already mapping their exposures and building their defenses. The window to do that proactively is still open. It will not stay open indefinitely.

Section IV | Frameworks for Preparation

The frameworks outlined here are designed to give a business owner the clarity and structure to navigate a turbulent cycle without being blindsided. The core objective is simple: keep the business alive, protect what has been built, and position for the opportunities that open up when unprepared competitors break.

The mental framework starts with an honest assessment. Every business has a unique operational rhythm, a specific set of vulnerabilities, and a finite pool of resources. The goal is not to implement every possible defensive measure simultaneously. The goal is to understand exactly where your business is exposed and build targeted responses to the highest-probability threats before they arrive.

Defense: Protect the Core

Cash is the foundation of everything. Without it, strategy is irrelevant. The first priority is understanding precisely how cash moves through the business: when it enters, when it exits, and where the timing gaps exist. An enterprise that can survive six months with zero incoming revenue has real operational freedom. One that is running on 30-day margins has none.

Audit your cash flow timing with clinical honesty. Map your accounts receivable aging against your fixed overhead schedule. Identify the exact window where a buyer payment delay would create a crisis and build a response protocol for that scenario before it happens. If your largest buyer represents 25% or more of revenue, that concentration is a structural risk regardless of how stable the relationship feels today.

Supply chain visibility is the second line of defense. Most operators manage two layers: their direct vendor and their direct buyer. The disruptions in this cycle are happening three and four tiers back. Audit your material inputs down to the sub-component level. Identify which components are sourced from overseas corridors exposed to maritime disruption, energy rationing, or tariff penalties. For any component that is both critical to fulfillment and sourced through a volatile corridor, stockpiling is a superior hedge to hoping the supply chain normalizes. A $5 component that grounds your entire production line is not a minor procurement detail. It is an existential risk.

Contractual vulnerabilities deserve the same audit. Review every active vendor and buyer agreement. Most contracts were written during stable conditions and do not contain force majeure language, renegotiation triggers, or extension clauses that account for the current environment. Identify your exposure on both sides before a disruption forces the conversation.

Internal operational integrity is the final layer of defense. Document your workflows. The businesses most vulnerable during a crisis are those where critical operational knowledge lives exclusively in the heads of two or three key people. If a key employee exits during a period of stress, the resulting disruption can be more damaging than the external threat itself. Standard operating procedures, cross-training, and documented processes are not administrative overhead. They are insurance.

Offense: Capture What Opens Up

Defense alone is not a survival strategy. The businesses that come through this cycle strongest are the ones that recognize the market disruption creates real opportunity. Unprepared competitors will break. Their clients will need alternatives. Their talent will become available. Their assets will go to market at distressed valuations.

The offensive posture is straightforward: expand your surface area with the market before the disruption hits your competitors, so that when their clients go looking for a stable alternative, your business is already visible and credible. This does not require massive marketing spend. It requires consistent, relevant signals to your target market that your operations are prepared, your supply lines are insulated, and your team is intact.

In B2B contexts, demonstrating operational competence and supply chain readiness to enterprise buyers is a direct competitive advantage right now. Buyers who have been burned by delivery failures are actively looking for vendors who can prove stability. In B2C contexts, the businesses that hold community trust and deliver consistent quality while competitors degrade their service will capture lasting loyalty at a fraction of normal acquisition cost.

The offensive play is secondary to a stable defense. Scaling into a fragile operational foundation accelerates failure. Get the foundation right first, then expand.

Network: Your Asymmetric Resource

In a stable economy, a business network is a convenience. In this environment, it is a structural advantage. Direct access to alternative capital sources, alternative vendors, and demand intelligence before you need them urgently is the difference between navigating a disruption and being destroyed by one.

The three pillars of a functional network in this cycle are capital, supply, and demand. Capital access means having established relationships with alternative private lenders, specialty finance providers, and non-bank credit sources before a liquidity crunch forces a rushed decision. A business that applies for structured credit from a position of stability gets dramatically better terms than one applying from a position of distress. Supply access means having identified and pre-qualified backup vendors for your highest-risk material inputs before a shortage forces a gray market purchase that compromises quality and triggers contract penalties. Demand access means knowing where the displaced buyer flow will go when competitors fail, and being positioned to receive it.

Building this network takes time, which is precisely why it needs to happen now rather than when the pressure arrives. The most valuable people in your corner are those who operate across domains: someone who understands capital structures and has direct access to both buyers and sellers within your market is a force multiplier. Finding those relationships before you need them is one of the highest-leverage actions available to an operator in this environment.

The Operational Baseline

Before any strategy is executed, run the following audit against your business:

Map every incoming macro threat vector that interacts with your sector and establish a response protocol for each. Review your real-time cash flow schedule, accounts receivable timing, and active contracts to identify where your margins are actually exposed. Audit your supply chain down to the sub-component level and flag every input sourced through a volatile corridor. Calculate your exact survival runway under a scenario where incoming revenue drops to zero. Align your core team around an honest assessment of current conditions so that if a defensive pivot becomes necessary, it is executed from a foundation of internal trust rather than reactive panic. Secure critical inventory reserves for your highest-risk components before market shortages force premium pricing. Establish direct lines to alternative capital before you need it urgently.

The operators who execute this baseline today will navigate this cycle from a position of clarity. The ones who wait for the disruption to make it obvious will be responding under duress with a depleted cash position and no time to build the relationships and reserves that take months to establish.

Conclusion

The 2026 environment is a structural realignment, not a temporary correction. The cracks forming across the banking system, global supply chains, energy markets, and consumer spending capacity will deepen through 2027 and into 2028. The businesses that survive and capture ground in this cycle share one defining characteristic: they acted before the pressure arrived at their door.

Fundamental demand is intact. Essential industries continue to operate. Capital continues to flow, even if the channels have shifted. The opportunity is real for operators who are prepared to receive it.

If this report identified exposures in your operation that you are not currently hedged against, that is the conversation worth having now.

The window to prepare proactively is still open. Use it.

About Eieyani Capital Associates

Eieyani Capital Associates is a boutique finance brokerage connecting businesses and capital sources to the right structures at the right time.

For businesses, we bring market intelligence, situational strategy, and access to capital facilities aligned to operational goals. Every engagement is built around both the capital and the structural clarity to deploy it effectively. For capital sources, we deliver prepared deal flow with the operational context and deployment strategy already engineered.

We act as the orchestrator between risk, opportunity, and capital for all stakeholders within the transaction.

References

[1] Congressional Research Service. (2026, March 11). Iran Conflict and the Strait of Hormuz: Impacts on Oil, Gas, and Other Commodities (CRS Report No. R45281). Congress.gov.

https://www.congress.gov/crs-product/R45281

[2] Office of the United States Trade Representative. (2026, June 9). Presidential tariff actions. Trade Topics Portal.

https://ustr.gov/trade-topics/presidential-tariff-actions

[3] Mortgage Bankers Association. (2026, March 2). Chart of the Week: Commercial Real Estate Loan Maturity Volumes. MBA Newsroom.

[4] International Energy Agency. (2026, June 4). 2026 Energy Crisis Policy Response Tracker: Explore government actions to conserve energy and support consumers in response to the energy market impacts of the conflict in the Middle East. IEA Data & Statistics Hub.

[5] Federal Reserve Bank of New York. (2026, May 12). Household Debt Balances Rise Slightly as Delinquency Transition Rates Hold Steady. New York Fed Press Center.

https://www.newyorkfed.org/newsevents/news/research/2026/20260512

[6] PwC. (2026, April 16). Capital reform 2026: Basel III endgame and more. PwC Financial Services Regulatory Library.

https://www.pwc.com/us/en/industries/financial-services/library/basel-iii-endgame.html

[7] Challenger, Gray & Christmas. (2026, June 4). Challenger Report: May Job Cuts Rise 16% from April; Highest May Total Since 2020. Challenger Gray Intelligence.

[8] Intercontinental Exchange. (2026, March 27). ICE Reports Record Market Activity as Customers Respond to Middle East Impacts. ICE Investor Relations.

[9] Consulting.us. (2026, April 17). Middle East war pushes supply chain pressures to three-year high. Consulting.us News.

[10] Bain & Company. (2026, February 22). Private Equity Outlook 2026: Gaining Traction. Bain Insights.

https://www.bain.com/insights/outlook-gaining-traction-global-private-equity-report-2026/

[11] Global Trade Alert. (2026, February 21). Section 122 in effect: What the US tariff regime looks like now. Global Trade Alert Reports.

https://globaltradealert.org/reports/S122-US-Tariff-Estimates

[12] U.S. Bureau of Industry and Security. (2026). Section 232 Inclusions Processes. U.S. Department of Commerce.

[13] Office of the United States Trade Representative. (2026, June 2). Report in Section 301 Investigations Acts, Policies, and Practices of Various Economies Related to the Failure to Impose and Effectively Enforce a Prohibition on the Importation of Goods Produced with Forced Labor. Executive Office of the President.

[14] Kearney. (2026, June 8). Why US manufacturing imports hit a four-year high despite record investment and tariffs 2026 Reshoring Index. Operations & Performance Insights.

https://www.kearney.com/service/operations-performance/us-reshoring-index

[15] Stanford University. (2026, February 25). Understand Crude Oil. Stanford Understand Energy Program.

https://understand-energy.stanford.edu/news/understand-crude-oil

[16] Brookings Institution. (2026, June 8).Iran war reverberations: A nadir for Asia’s economic security. Brookings Global Economy & Development.

https://www.brookings.edu/articles/iran-war-reverberations-a-nadir-for-asias-economic-security/

[17] New Statesman. (2026, March 21). The world energy shock is coming. New Statesman Geopolitics.

https://www.newstatesman.com/international-politics/geopolitics/2026/03/the-world-energy-shock-is-coming

[18] Food and Agriculture Organization. (2026, March 15). GLOBAL AGRIFOOD IMPLICATIONS OF THE 2026 CONFLICT IN THE MIDDLE EAST. FAO Knowledge Repository.

[19] National Restaurant Association. (2026, May 29). Same-store sales and customer traffic. Research & Media Hub.

[20] Franklin Templeton. (2026, April 9). The evolution of private credit. Franklin Templeton Alternatives Insights.

https://www.franklintempleton.lu/articles/2026/alternatives/the-evolution-of-private-credit

[21] With Intelligence. (2026). Private credit outlook 2026: The market faces its first big test. With Intelligence Compendium Series.

https://www.withintelligence.com/insights/private-credit-outlook-2026/

Disclaimer

This document is provided solely for informational and educational purposes. It does not constitute financial, lending, legal, tax, investment, accounting, or professional advice of any kind, and must not be relied upon as such.

The information contained herein is based on publicly available sources believed to be reliable at the time of publication. Eieyani Capital Associates makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of any information herein. All information, opinions, estimates, and forward-looking statements are as of the date of publication and are subject to change without notice. The strategies, frameworks, scenarios, and examples described in this document are illustrative and general in nature. They do not account for your specific business circumstances, financial condition, credit profile, industry, or regulatory environment. All examples are hypothetical and provided for conceptual purposes only.

Nothing in this document establishes any client, advisory, broker, fiduciary, or agency relationship between the reader and Eieyani Capital Associates or any of its affiliates. Nothing herein constitutes a recommendation to enter into any financing, credit, or contractual arrangement, nor does it guarantee funding, approval, specific rates, terms, outcomes, or financial performance of any kind. All business, financial, and credit decisions involve risk. Readers are solely responsible for their own due diligence and are strongly encouraged to consult qualified, licensed professionals before acting on any information contained herein.

Eieyani Capital Associates and its affiliates expressly disclaim all liability for any direct, indirect, incidental, or consequential loss or damage arising from the use of, reliance on, or interpretation of this document or any portion thereof.

© 2026 Eieyani Capital Associates. All rights reserved. No part of this publication may be copied, reproduced, distributed, or transmitted in any form or by any means without the prior written permission of Eieyani Capital Associates.